- Blogs

- /

- What Happens if You Cannot Pay Taxes? 5 Steps You Must Know

What Happens if You Cannot Pay Taxes? 5 Steps You Must Know

Summary

‘Nothing is certain except death and taxes.’ — Benjamin Franklin.

You may be surprised to know that Benjamin Franklin made this quote in 1789, and it still holds today.

In 2022, the US government collected $2.6 trillion in income taxes. That’s about 52% of the total revenue it generated.

Let’s face it, taxes remain the primary source of income for most governments, and failing to pay them can lead to severe consequences.

The IRS doesn’t care if you cannot pay taxes due to hardship, oversight, or other reasons. They will garnish wages, seize assets, or put a lien on property if you owe taxes and aren’t trying to pay.

These consequences often escalate if you don’t address them. That’s why we’d be showing you what happens if you cannot pay taxes and how you can soften the impact and regain your financial stability.

Key Takeaways

- Failing to pay your taxes by the deadline attracts penalties and interest charges that compound with time.

- If your taxes are unpaid for 3-6 months, you risk getting a lien on your property, wage garnishment, or facing criminal charges.

- You can resolve your tax debt by filing on time, negotiating payments with the IRS, or getting help from a tax professional.

- Consider exploring installment agreements or short-term extensions to structure your tax repayment and ease the burden of making lump-sum payments.

- Consider paying your taxes with a credit card or personal loan. But ensure you consider their terms and interest rates.

- The IRS can send your unpaid taxes to collection agencies, which could impact your credit score.

What Happens if You Cannot Pay Taxes

The IRS takes taxes seriously. Here’s a breakdown of what happens if you can’t pay your taxes after Tax Day:

Immediately After Tax Day

If you fail to pay your taxes by the deadline—typically April 15 if you live in the United States—you’ll face penalties and interest charges.

These penalties can include a failure-to-pay penalty, which is generally 0.5% of your monthly unpaid taxes. If ignored, this penalty maxes out after 50 months and can hit 25% of your unpaid taxes.

But it gets worse because if you failed to file your taxes before tax day, you’d be slammed with a failure-to-file penalty. This penalty means you’d be fined 5% of the unpaid taxes for every day your tax payment is late.

Some people make the wrong choice of not paying their taxes because they don’t have the complete amount.

But this is a dangerous decision because failing to file and pay your taxes dramatically increases your tax burden. And that’s because the IRS charges interest on the unpaid balance.

The IRS will send you a notice showing how much you owe, including penalties and interest. This notice serves as a reminder of your outstanding tax debt and usually informs you of the consequences of non-payment.

1-3 Months After Tax Day

The penalties and interest will accumulate if you still haven’t paid your taxes within the first few months after Tax Day. And yes, this can significantly increase the total amount you owe.

Let’s say you live in New York and pay $18,000 in taxes yearly. But for whatever reason, if you only paid off your taxes six months after tax day, you’d have to pay over $18,670. That’s an additional $670 in compounding interest.

And if you decide to leave your taxes unpaid till the next tax day. You could end up paying thousands in interest and penalties.

Also, it’s worth noting that you’ll keep receiving mails from the IRS, reminding you of how much you owe and warning you of the consequences if you refuse to clear your tax debt.

3-6 Months After Tax Day

After several months of non-payment, the IRS may take things a step further by taking more aggressive actions to recover the unpaid taxes. How would they do that?

First, the IRS may place a tax lien on your property. A lien is a legal claim against your assets to secure the payment of your tax debt. A tax lien on your credit report can negatively impact your credit score and affect your ability to sell or refinance your property.

They could also initiate wage garnishment or bank levies to collect the unpaid taxes. With wage garnishment, the IRS deducts money directly from your paycheck, while a bank levy allows the IRS to seize funds from your bank account.

3+ Months After Tax Day

If you continue to ignore or delay your tax payment, the IRS may take more drastic actions, like seizing your assets to satisfy the outstanding tax debt. And yes, they can seize your home, bank accounts, cars, or any other valuable property.

But it gets worse because once the IRS classifies your unwillingness to pay as deliberate non-compliance or tax evasion, they’ll fine criminal charges against you. This legal action can lead to fines, extreme penalties, or even imprisonment.

And one thing folks who refuse to pay their taxes forget is that failing to address their tax obligations can have long-term financial consequences. It can affect your credit score, make it difficult to get a loan, lead to loss of assets, and trigger severe legal ramifications.

That’s why you must address your tax debt promptly and get help from tax professionals or the IRS if you cannot pay on time.

Here’s What You Can Do if You Owe Back Taxes

Step 1: Always File Your Taxes

Always file your taxes before the deadline, even if you can’t pay the full amount owed. Doing this is crucial because the IRS imposes penalties when you don’t file. The failure-to-file penalty can be much higher than the penalties for failure-to-pay.

The beauty of filing on time is that you give yourself enough time to pay. Plus, you can avoid extra fees and comply with tax laws.

Now, one question we often get from folks is, ‘What if I filed a tax extension?’ Well, filing a tax extension doesn’t mean you won’t get to pay your tax on Tax Day.

It just means you won’t get charged with failure-to-pay penalties. But you would still get charged a 0.5% late payment fee, which maxes out at 25% of your tax bill.

Step 2: Pay as Much as You Can Before the Tax Deadline

If you cannot pay the total taxes you owe, try to pay as much as possible before the tax deadline. Doing this reduces the overall amount you’ll get fined in terms of interest and penalties.

Even partial payments demonstrate your commitment to meeting your tax obligations and may help mitigate the consequences of late payments.

Step 3: Contact the IRS About a Payment Plan

Don’t hesitate to visit the IRS’s website to apply for a payment plan if you cannot fully pay your taxes by the deadline.

The IRS offers various payment plans, including short-term extensions and long-term installment agreements, to help taxpayers manage their tax debts.

When you apply for a payment plan and it gets approved, the IRS suspends collecting your taxes for a specific duration and won’t apply any levies.

With the short-term extension, you get an extra 180 days to pay your taxes. Meanwhile, with the long-term installment agreement, you’ll get to pay off your taxes in monthly installments. Taking advantage of these options early can help you avoid accumulating extra penalties and interest.

However, if your application for a payment plan gets rejected, the IRS suspends collecting your taxes for 30 days.

Step 4: Get Help From a Tax Professional

Tax issues can be complex, especially when dealing with back taxes and payment plans. That said, the best thing you can do is get valuable expertise and guidance from a qualified tax professional like a tax attorney or certified public accountant (CPA).

Tax professionals can assess your financial situation, negotiate with the IRS on your behalf, and ensure you take advantage of all available options for resolving your tax debt.

Five Options That’d Help You Pay Your Taxes

1. Get a Personal Loan

If you don’t have enough funds to pay your taxes, consider taking out a personal loan to cover the tax debt.

Personal loans are some of the best ways to access funds with fixed monthly payments and interest rates quickly.

Besides taking a personal loan from a bank or credit union, you should also consider using a home equity loan or line of credit or borrowing from a retirement account like your 401(k) or IRA.

But before applying for a personal loan, compare loan options from different lenders to find the best terms and rates for your financial situation. Be sure to consider the total cost of the loan, including interest and fees, before borrowing.

Also, consider your loan’s interest rates, fees, and repayment terms. Doing this will help you pick the best loan option for your financial situation.

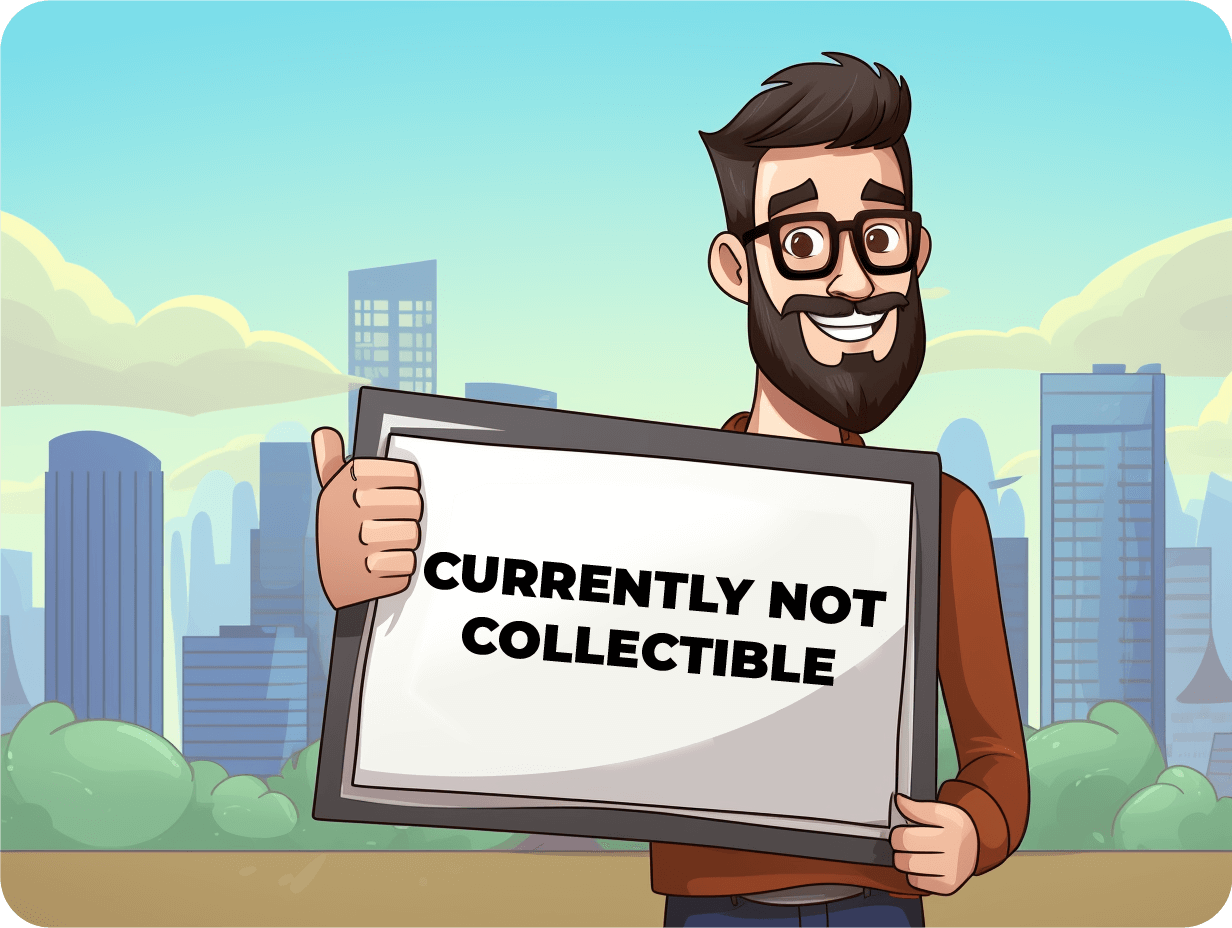

2. Apply for a Currently Not Collectible Status

One great option if you’re experiencing financial hardship and cannot pay your taxes is to apply for a ‘currently not collectible’ (CNC) status with the IRS.

This status temporarily suspends IRS collection efforts due to your inability to support yourself and pay taxes. To qualify for CNC status, you must demonstrate that paying your tax debt would cause significant financial hardship.

Although getting a CNC status can give you temporary relief from the IRS’s collection activities, your unpaid taxes would continue to accrue interest and penalties.

3. Get a Settlement

In certain circumstances, you can negotiate a settlement with the IRS to resolve your tax debt for less than the full amount owed.

This option, known as an offer in compromise (OIC), allows you to settle your tax liability for an agreed-upon lesser amount. When applying for an OIC, you must complete forms 433-A and 656, pay a $205 application fee, and an initial payment towards your new tax balance.

To qualify for an OIC, you must meet specific eligibility criteria and demonstrate that paying the full tax debt would create a significant financial hardship.

Yes, an OIC can provide a fresh start if you’re struggling with tax debt, but ensure you get professional advice before pursuing this option.

4. Pay With a Credit Card

If you cannot pay your taxes with cash or other means, you can use a low annual percentage rate (APR) credit card to cover the tax debt.

The IRS accepts credit card payments through authorized payment processors, but know that using a credit card can attract additional fees, like convenience or interest charges, if you carry a balance.

Before using a credit card to pay your taxes, consider the costs and benefits compared to other payment options.

5. Use Your Emergency Funds

If you have savings set aside for emergencies, you should use these funds to pay your taxes. Don’t make the same mistakes as some folks who’d rather pay the IRS’s interest and penalties than use their emergency funds to clear their tax debt.

Although it’s crucial to maintain an emergency fund for unexpected expenses, paying taxes is also a financial obligation that should be prioritized. But ensure you’ve considered every other option before using your emergency funds.

8 Tax Scams You Should Watch For

Over 75,000 unsuspecting Americans have lost over $28 million to scams where criminals pretend to be IRS representatives while collecting their personal information and sometimes their tax refunds.

Here are the common tax scams you should watch for:

1. Phishing Scams

Always be cautious of unsolicited emails, text messages, or phone calls claiming to be from the IRS or tax authorities. These messages often contain requests for personal or financial information, like your Social Security number or bank account details.

Remember, the IRS will never contact you via email, text, or social media to request sensitive information. So, view any communication between you and the supposed IRS on these channels as scams.

2. Impersonation Scams

Scammers may impersonate IRS agents or other tax officials over the phone, demanding immediate payment of alleged tax debts or threatening legal action like arrest, wage garnishment, or even deportation.

Remember that legitimate tax authorities will never threaten you with arrest or deportation or demand payment without providing an opportunity to question or appeal the amount owed.

3. Fraudulent Tax Preparers

Watch out for ‘tax experts’ who promise to get large refunds or offer to prepare your taxes for an unreasonably low fee.

These scammers know tons of people struggle with their tax debt, and they won’t hesitate to make extraordinary claims just to get you to pay them for a service they’ll never perform.

And yes, these fraudulent tax preparers may use deceptive tactics to manipulate your tax return or claim false deductions or credits, which could result in penalties or legal consequences for you.

4. Fake Charities

During tax season, scammers may create fake charities or bogus fundraising schemes to solicit donations from well-meaning folks.

These fraudulent organizations often use names similar to legitimate charities. They could even use high-pressure persuasion tactics to solicit donations.

So, before making any donations during tax season, you research the organization to ensure it’s legitimate and tax-exempt.

5. Identity Theft and Refund Fraud

Identity thieves may use stolen personal information, like your Social Security number or tax identification number, to file fraudulent tax returns and claim refunds in your name. These scammers often target low-income folks or those not required to file tax returns.

To protect yourself from identity theft and prevent refund fraud, safeguard your personal information, file your tax return as early as possible, monitor your credit report, and quickly report any suspicious activity to the IRS.

6. Fake Tax Software

Be careful when downloading tax preparation software or accessing tax-related websites, as some may be fraudulent or contain malware designed to steal your personal information. Always stick to reputable software providers and official IRS websites when filing your taxes online.

7. Social Security Number Scams

Some scammers may claim that your Social Security number has been suspended due to suspicious activity or unpaid taxes. They may instruct you to provide sensitive information or make immediate payments to resolve the issue.

Remember that the Social Security Administration will never suspend your Social Security number, and legitimate government agencies will not demand payment over the phone or via email.

To avoid falling victim to tax scams, remain vigilant and stay updated on the tactics scammers use. If you suspect something is wrong, report it immediately to the IRS or the Federal Trade Commission (FTC).

Remember, only consult with a trusted tax professional or financial advisor if you have concerns about your tax situation or encounter suspicious communication regarding your taxes.

Freedom From Unpaid Taxes

The consequences of being unable to pay taxes can be challenging. Still, you can take several actionable steps to address your tax debt and stop its effect from further straining your financial strain.

By understanding the immediate and long-term implications of unpaid taxes and using excellent resources like setting up a payment plan, professional assistance, and alternative borrowing options, you can make it out of any challenging tax situation with greater confidence and control.

Remember, always maintaining timely communication with the IRS, staying honest about your financial circumstances, and making proactive plans can help you resolve any tax-related challenges.

So, don’t delay; start taking decisive action and pushing yourself towards a more secure financial future, free from the burden of unpaid taxes.

FAQs

What happens if you cannot pay taxes?

If you cannot pay taxes, you may face penalties like fines, interest charges, and even legal actions such as wage garnishment or property seizure.

Communicating with tax authorities is crucial to explore options and prevent escalating consequences.

How can I request an extension to pay back taxes?

To request a payment extension for owing back taxes, contact the tax agency promptly. They may grant extra time based on your circumstances.

Be proactive in reaching out and explaining your situation to avoid additional penalties.

What is an Offer in Compromise for tax payments?

An Offer in Compromise is a settlement option where you negotiate with the IRS to pay less than you owe.

It involves proving financial hardship or exceptional circumstances that make full payment challenging. Consider this route if meeting your tax obligations seems impossible.

Can I suspend collections if I can’t afford to pay my taxes immediately?

You can suspend collections temporarily by demonstrating financial hardship or other valid reasons.

This pause gives you breathing room while exploring alternative payment arrangements. Contact the tax agency promptly to discuss suspension options tailored to your situation.

Are there borrowing options available to make tax payments?

Yes, borrowing options like personal loans or using credit cards exist to pay off taxes owed.

However, carefully weigh the interest rates and terms before deciding on this approach. Explore all alternatives first before committing to borrowing as a solution.

Our Latest Blogs:

FREE Strategy Session to Fix Your Credit Blogs / A statement balance is the total amount of money a...

ThisIsJohnWilliams

CEO of GreatCreaditFast.com

FREE Strategy Session to Fix Your Credit Blogs / Facebook Twitter Linkedin Instagram Share Summary Life can be unpredictable...

ThisIsJohnWilliams

CEO of GreatCreaditFast.com

FREE Strategy Session to Fix Your Credit Blogs / Facebook Twitter Linkedin Instagram Share Summary Did you know that...

ThisIsJohnWilliams

CEO of GreatCreaditFast.com

FREE Strategy Session to Fix Your Credit Blogs / Facebook Twitter Linkedin Instagram Share Summary Becoming a homeowner is...

ThisIsJohnWilliams

CEO of GreatCreaditFast.com

FREE Strategy Session to Fix Your Credit Blogs / Facebook Twitter Linkedin Instagram Share Summary How to recover from...

ThisIsJohnWilliams

CEO of GreatCreaditFast.com

Knowing how to survive a recession is vital to thriving despite complex financial challenges. Here’s everything you must know....

ThisIsJohnWilliams

CEO of GreatCreaditFast.com